Three letters like AAA, BBB+, or D can quietly shape the future of a business. They influence whether funding is available, how expensive that funding becomes, and how confidently banks, investors, and other stakeholders engage with a company. Despite their importance, credit ratings are often misunderstood and reduced to a compliance requirement rather than being seen for what they truly are.

So what do credit ratings really mean?

At their core, credit ratings represent an informed and independent opinion. They assess the likelihood that a borrower will meet its financial obligations fully and on time. A credit rating is not a promise or a guarantee of repayment. It is a structured assessment based on financial data, qualitative evaluation, and professional judgment. In many ways, credit ratings act as a shared language of trust that allows lenders, investors, and regulators to make decisions using a common reference point.

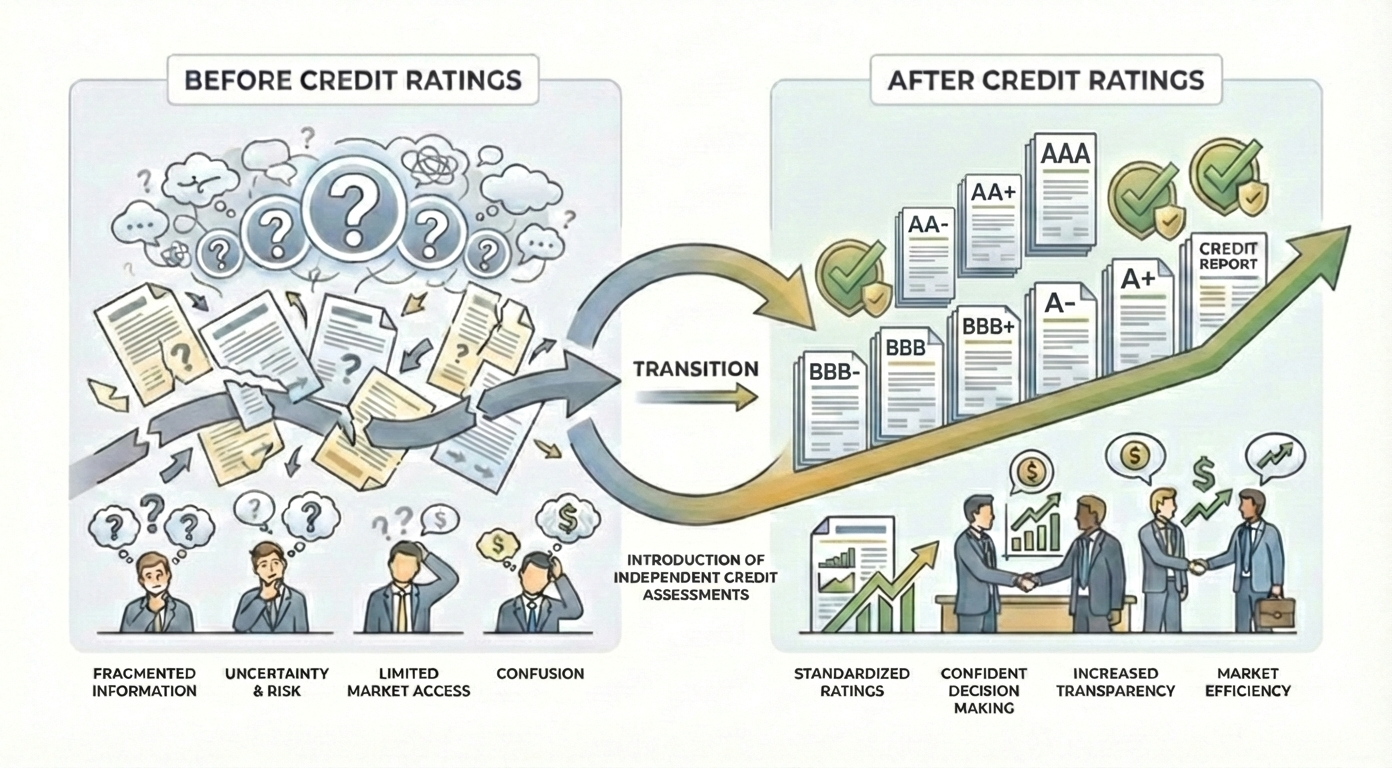

Before credit ratings existed, lending decisions were far more complex and uncertain. Financial information was fragmented, disclosure standards were inconsistent, and comparing one borrower with another was difficult. Credit ratings emerged to bridge this gap by bringing standardisation and transparency to credit assessment. They made it possible to evaluate risk more objectively and to take lending and investment decisions with greater confidence and speed.

For lenders and investors, credit ratings offered a clearer understanding of default risk. For companies, they created a pathway to better access to capital. A strong credit profile often translates into lower borrowing costs, improved credibility, and broader funding options. Over time, credit ratings became an essential part of how capital flows through the financial system.

In India, the credit rating framework began taking shape in 1987 with the establishment of the country’s first rating agency. What started as a limited initiative focused on corporate debt gradually expanded across products and sectors. Today, credit ratings cover bank loans, commercial papers, fixed deposits, structured instruments, and large project finance exposures. They have evolved into a critical component of India’s financial architecture, influencing almost every significant lending and investment decision.

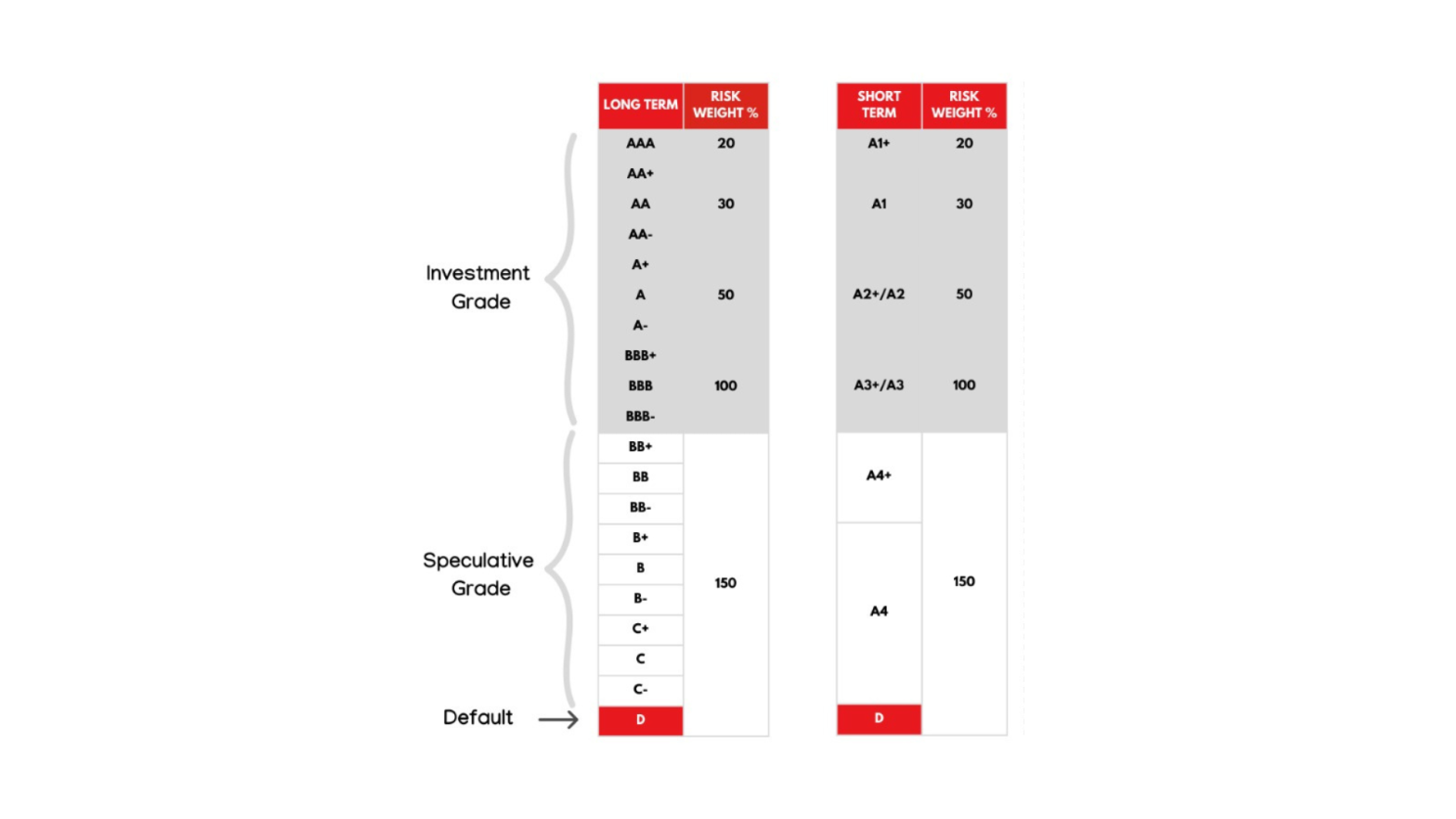

A credit rating symbol such as AAA, BBB+, or D is a concise summary of credit risk. Higher ratings indicate a stronger ability to service debt, while lower ratings suggest higher vulnerability. While these symbols appear simple, the analysis behind them is extensive. Rating agencies examine financial performance, cash flow stability, business models, industry dynamics, management capability, governance practices, and future projections. A credit rating therefore reflects both numbers and judgment, combining quantitative data with qualitative insights.

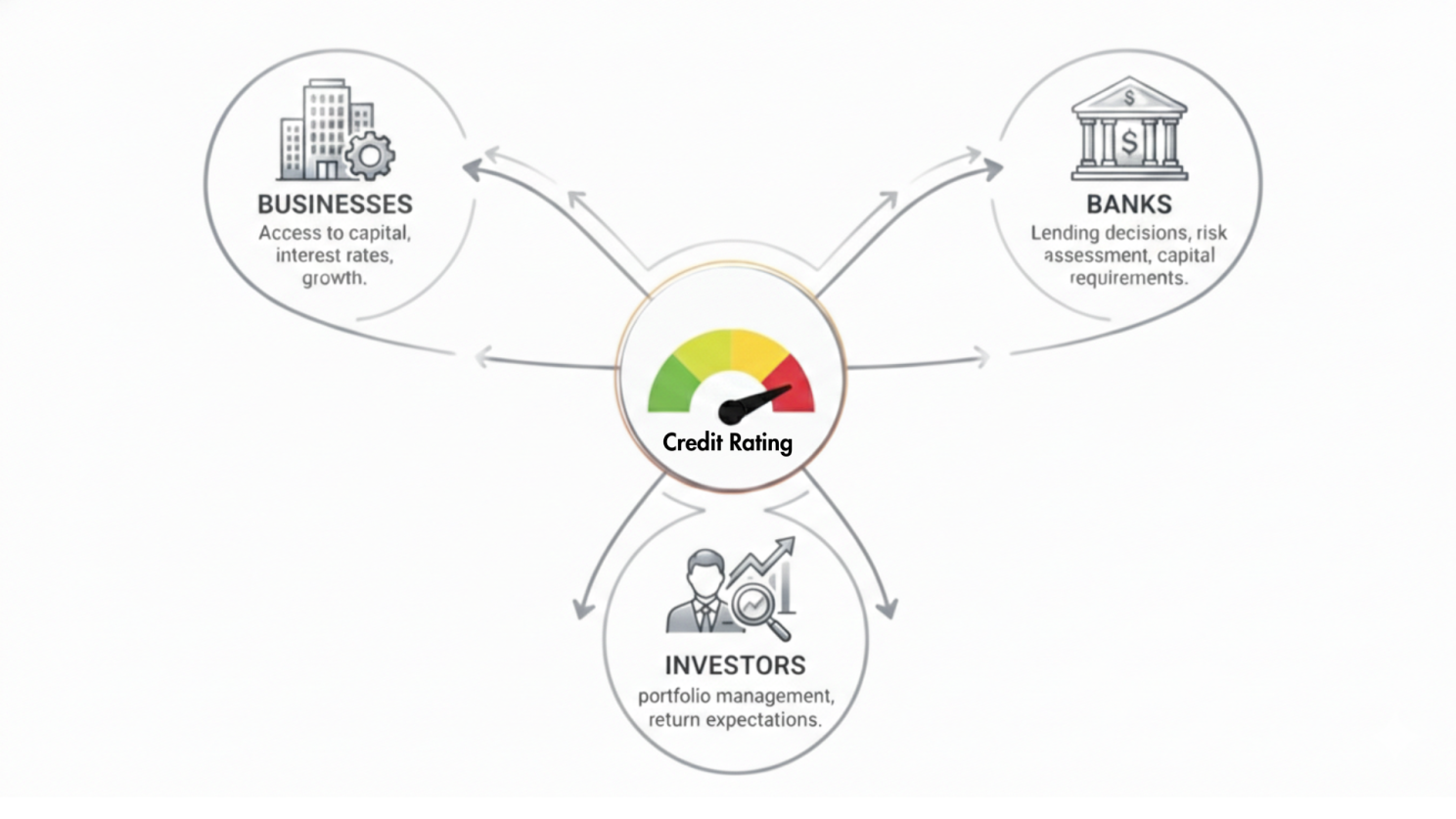

The impact of credit ratings extends far beyond individual companies. Businesses are affected through borrowing costs, loan approvals, and market perception. Investors rely on ratings to compare risk across instruments and issuers. Banks use them as a key input in credit appraisal and capital planning. Regulators depend on ratings to strengthen discipline and stability within the financial system. In this way, credit ratings quietly influence the efficiency and integrity of the entire financial ecosystem.

Ultimately, a credit rating is not just a label attached to a balance sheet. It is a reflection of how a business is viewed in terms of financial discipline, resilience, and credibility. Understanding what a rating represents is the first step toward managing it effectively. When businesses understand their ratings, they move beyond acceptance and begin to focus on strengthening fundamentals, communicating their strengths more clearly, and building long term trust with stakeholders.

Credit ratings may be expressed in just a few letters, but the story behind them is far deeper. Understanding that story is essential for anyone who participates in the world of finance.