Unlocking Massive CC Limits: How Andheri’s Manufacturers Use Credit Ratings to Improve Liquidity

By: admin

Articles

Unlocking Massive CC Limits: How Andheri’s Manufacturers Use Credit Ratings to Improve Liquidity

In the industrial clusters of Andheri, manufacturing businesses operate in a constant cycle of production, dispatch, and receivables.

Growth is rarely constrained by demand. It is constrained by liquidity.

For many manufacturers, the difference between stagnation and scale lies in one critical factor: the size and flexibility of their Cash Credit (CC) limits.

What many CFOs and promoters overlook is that credit rating plays a decisive role in unlocking higher CC limits and improving working capital efficiency.

Why CC Limits Are Critical for Manufacturers

Manufacturing businesses are inherently working capital intensive.

They deal with:

High inventory holding

Delayed receivables

Continuous procurement cycles

Cash Credit limits act as the primary liquidity buffer, enabling companies to:

Fund day-to-day operations

Manage supplier payments

Execute larger orders without stress

However, CC limits are not just based on turnover or collateral. They are heavily influenced by risk perception, where credit rating plays a key role.

How Banks Decide Your CC Limit

Banks assess multiple parameters before sanctioning or enhancing CC limits:

Financial strength and net worth

Working capital cycle

Past banking conduct

Industry outlook

Credit rating

Credit rating acts as a third-party validation of creditworthiness, making lenders more confident in extending higher exposure.

A stronger rating signals:

Lower default risk

Better financial discipline

Higher repayment capability

This directly translates into higher sanctioned limits and better utilization flexibility.

The Andheri Manufacturing Advantage

Manufacturers in Andheri operate in a highly competitive and financially active ecosystem.

They benefit from:

Access to multiple banking relationships

Proximity to financial institutions

Faster credit decision cycles

In such an environment, well-rated companies stand out immediately, often receiving preferential treatment in:

Limit enhancements

Renewal approvals

Additional working capital facilities

From Rating to Liquidity: The Direct Link

Most businesses view credit rating as relevant only for term loans. In reality, it has a direct impact on working capital limits.

Here’s how:

A higher credit rating improves lender confidence, which encourages banks to:

Increase drawing power

Sanction higher CC limits

Reduce margin requirements in some cases

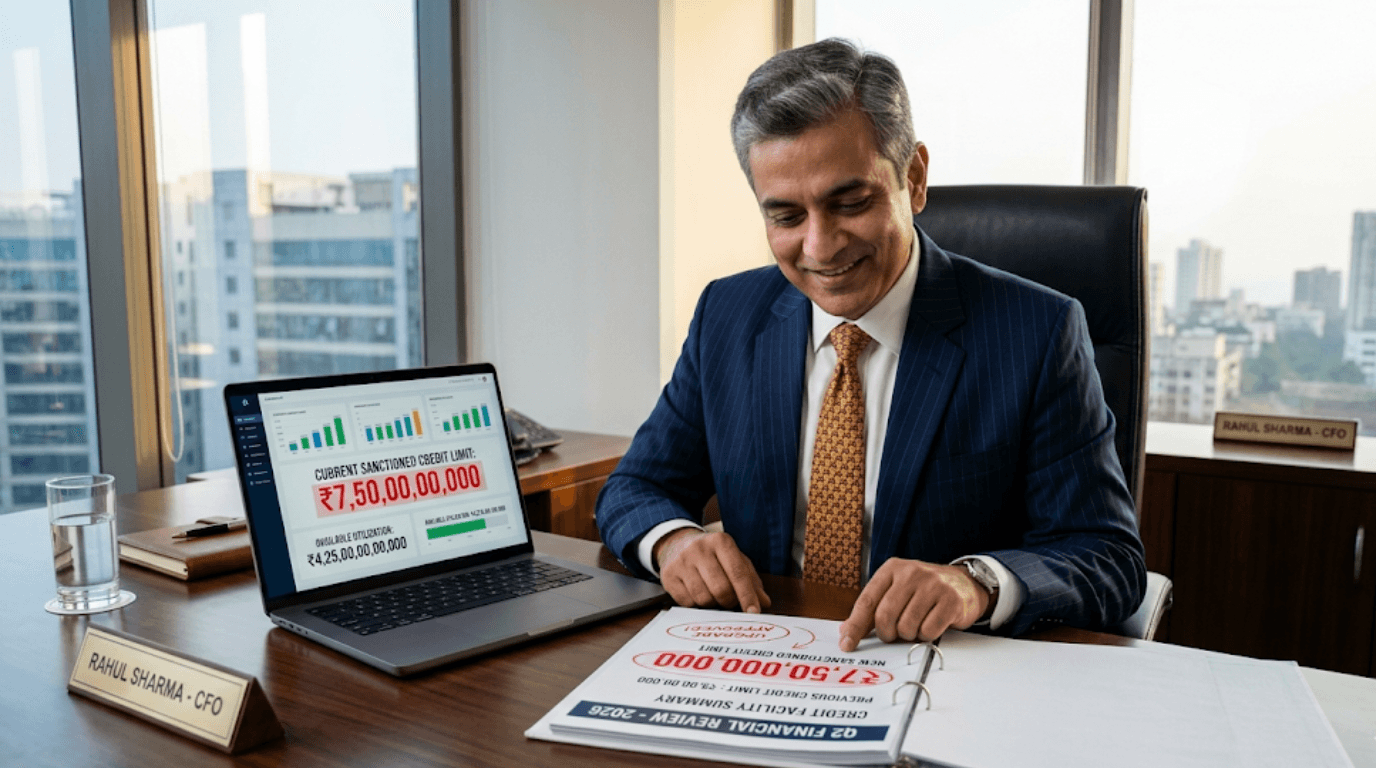

For example:

A manufacturing company with:

₹50 crore turnover

Moderate working capital cycle

May initially receive a CC limit of ₹8–10 crore.

After a rating upgrade:

The same company can justify a higher limit based on improved risk perception

Banks may enhance limits to ₹12–15 crore depending on overall profile

This additional liquidity can directly support:

Higher production capacity

Bulk raw material procurement at better pricing

Faster execution of large orders

Beyond Limits: Additional Benefits of a Strong Credit Rating

A better rating does not just increase the limit size. It improves the overall quality of working capital access.

Lower Interest on CC Utilization

Higher-rated companies often get finer pricing on working capital borrowings

Reduced Collateral Pressure

Stronger profiles may negotiate more favorable collateral structures

Faster Sanctions and Renewals

Banks process proposals quicker for well-rated borrowers

Stronger Banking Relationships

Improved credibility enhances trust with lenders

What Holds Back CC Limit Enhancement

Many manufacturers in Andheri face challenges not because of weak business fundamentals, but due to:

Poor financial structuring

Inefficient working capital management

Lack of clarity in presenting financial data

Under-communication of business strengths

In many cases, the issue is not performance. It is positioning.

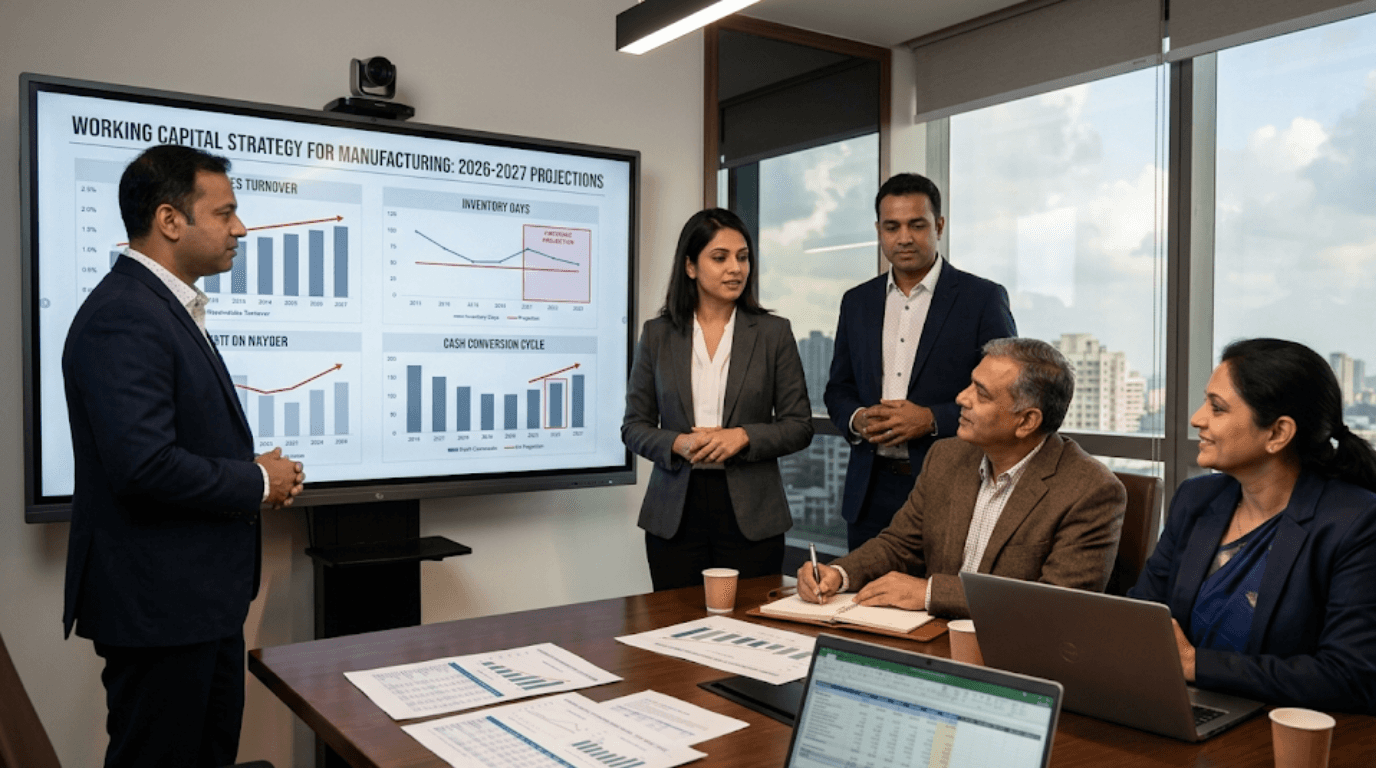

Strategic Levers to Improve CC Limits

Manufacturers looking to unlock higher liquidity should focus on:

Improving Financial Ratios

Strengthening leverage, current ratio, and coverage metrics

Optimizing Working Capital Cycle

Reducing receivable days and managing inventory efficiently

Strengthening Banking Conduct

Maintaining disciplined utilization and timely repayments

Enhancing Financial Transparency

Providing structured and timely financial information

Positioning for Rating Upgrade

Ensuring strengths are clearly communicated to rating agencies

The Strategic Insight Most Promoters Miss

Banks do not just fund numbers. They fund confidence.

Credit rating bridges the gap between internal performance and external perception.

Two manufacturers with similar turnover can have vastly different CC limits simply because one is better rated and better positioned.

Conclusion: Liquidity is a Strategy, Not a Constraint

In a competitive hub like Andheri, access to working capital can define growth trajectory.

A higher CC limit is not just additional funding. It is:

Operational flexibility

Negotiation power with suppliers

Ability to scale without disruption

A strong credit rating transforms liquidity from a constraint into a strategic advantage.

Why Companies Choose FinMen Advisors for Credit Rating Advisory

In working capital-intensive industries like manufacturing, unlocking higher CC limits requires more than financial strength. It requires the ability to present that strength effectively to lenders and rating agencies.

FinMen Advisors brings a structured and experience-driven approach to this process.

With over 15 years of specialized expertise, the firm understands how credit rating directly impacts working capital funding and bank negotiations.

Having executed more than 6,500 assignments, it has strong experience in aligning business profiles with lender expectations.

Its pan-India presence and established relationships with financial institutions enable better positioning during CC limit discussions.

The Prepare, Position, Protect approach ensures that companies are not only financially ready but also strategically presented.

A no-cost initial assessment helps businesses identify gaps in their credit profile and quantify the potential upside in liquidity.

Each engagement is customized to align with the company’s operational cycle, industry dynamics, and growth plans.

The Bottom Line

For manufacturers, liquidity is the backbone of growth.

Credit rating is one of the most powerful tools to enhance that liquidity.

With the right strategy and advisory support, businesses can unlock higher CC limits, improve financial flexibility, and scale with confidence.