Negotiating with Mumbai Banks: Using Credit Ratings to Hedge Against Rising Interest Rates

By: admin

Articles

Negotiating with Mumbai Banks: Using Credit Ratings to Hedge Against Rising Interest Rates

In the dynamic financial environment of Mumbai, interest rates are no longer stable variables. They are moving targets.

For CFOs, the challenge is not just borrowing capital, but protecting the cost of that capital in a rising or volatile interest rate cycle.

One of the most underutilized tools in this negotiation is credit rating.

Used strategically, credit rating is not just a reflection of risk. It becomes a negotiation lever that can hedge against rising interest rates.

Why Interest Rate Risk is a Real Concern for CFOs

India’s lending environment is witnessing:

Fluctuating policy rates

Changing liquidity conditions

Narrowing spreads between loans and bonds

Corporate borrowing patterns are shifting as companies actively evaluate the cost differential between bank loans and other funding sources.

At the same time, interest rate transmission is not uniform. The actual borrowing cost depends heavily on borrower-specific risk premium, not just benchmark rates.

This is where credit rating becomes critical.

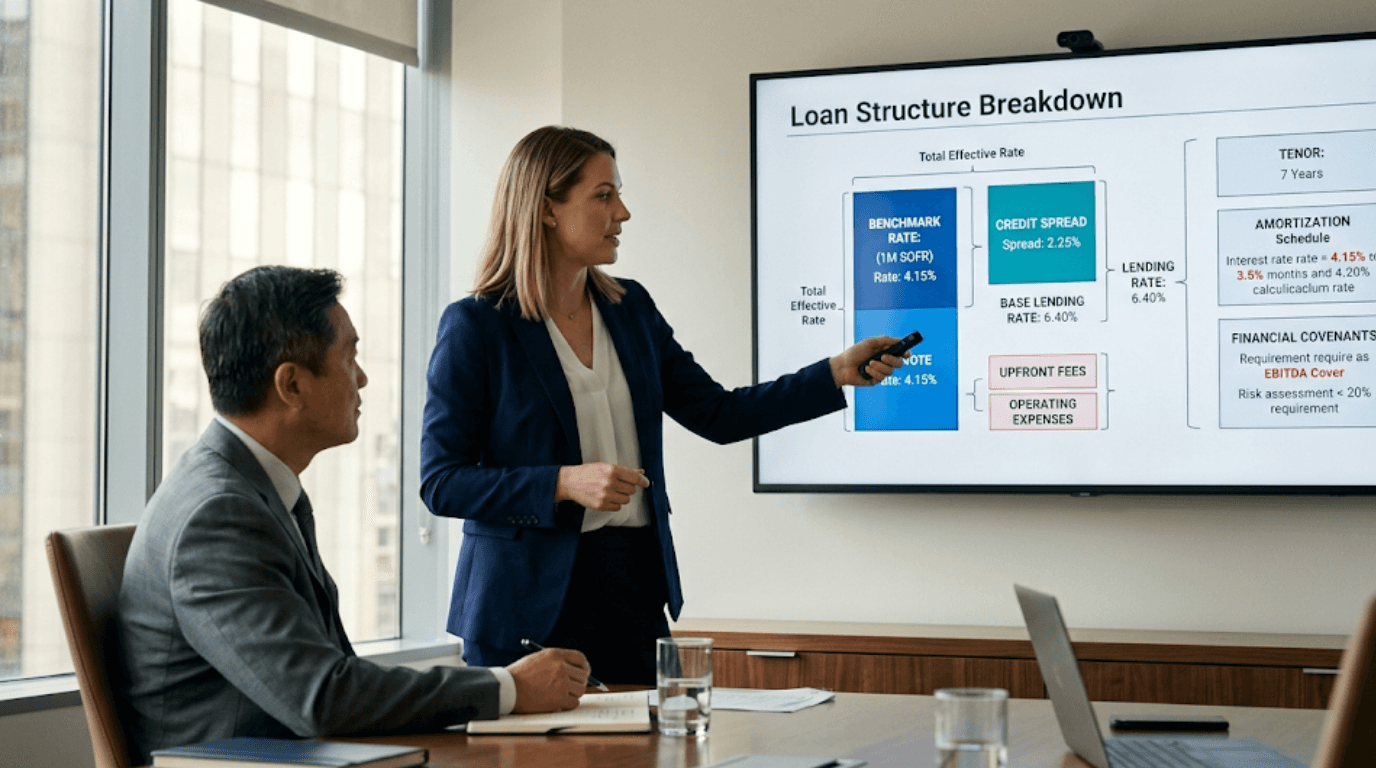

How Banks Actually Price Your Loan

Banks do not lend at a flat rate. They price loans using:

Final Interest Rate = Benchmark Rate (MCLR/Repo-linked) + Credit Spread

The credit spread is where negotiation happens.

And that spread is directly influenced by your credit rating.

Higher-rated companies are seen as lower-risk borrowers and therefore:

Get tighter spreads

Enjoy better pricing

Have stronger negotiation leverage

In fact, companies with higher ratings often extract finer pricing from banks due to their stronger bargaining position.

Credit Rating as a Hedge Against Rising Rates

Most CFOs focus on negotiating the base rate. The smarter ones focus on locking in lower spreads.

Here’s why:

When interest rates rise:

Benchmark rates increase for everyone

But credit spreads remain relatively stable for strong borrowers

This means:

A higher credit rating protects you from disproportionate cost increases.

For example:

Company A (BBB rated) sees spread increase during tightening cycles

Company B (A rated) maintains tighter spreads

Over time, this difference compounds into significant cost savings.

The Mumbai Advantage in Negotiation

Companies operating in Mumbai benefit from:

Access to multiple lenders (PSU banks, private banks, NBFCs)

Competitive loan pricing environment

Active refinancing and restructuring opportunities

As corporate lending grows and competition among lenders increases, well-rated borrowers are in a stronger position to negotiate favorable terms.

Beyond Pricing: What You Can Negotiate Using Credit Rating

A strong credit rating gives CFOs leverage beyond just interest rates.

You can negotiate:

Lower Credit Spread

Direct reduction in borrowing cost

Flexible Covenants

Less restrictive financial conditions

Longer Tenure

Better cash flow planning

Higher Sanction Limits

Improved access to capital

Faster Approvals

Reduced friction in credit processes

What Banks Look for During Negotiation

Banks evaluate borrowers based on:

Financial strength and leverage

Cash flow predictability

Industry outlook

Management quality

Credit rating acts as a summarized risk indicator, helping lenders make faster and more confident decisions.

Strategic Playbook for CFOs

To use credit rating effectively as a negotiation tool:

1. Know Your Rating Position

Understand where you stand and what is holding your rating back

2. Quantify the Spread Impact

Translate rating improvement into basis point savings

3. Time Your Negotiation

Approach lenders post-rating upgrade or during refinancing cycles

4. Create Competitive Tension

Engage multiple lenders to improve pricing

5. Strengthen Your Narrative

Clearly communicate business strengths and financial resilience

The Strategic Insight Most CFOs Miss

Interest rates are external.

Credit spreads are negotiable.

And credit rating sits at the center of that negotiation.

Two companies borrowing at the same time can end up with very different costs of capital—not because of market conditions, but because of how they are perceived by lenders.

Conclusion: Control What You Can

In a rising interest rate environment, CFOs cannot control macroeconomic cycles.

But they can control:

How their company is perceived

How risk is evaluated

How effectively they negotiate

A strong credit rating is not just a financial metric. It is a strategic hedge.

Why Companies Choose FinMen Advisors for Credit Rating Advisory

In a market where borrowing costs are increasingly sensitive to risk perception, the ability to position your credit profile effectively becomes a competitive advantage.

FinMen Advisors brings a structured and experience-driven approach to this process.

With over 15 years of specialized expertise, the firm has deep insight into how banks and rating agencies evaluate borrowers.

Having executed more than 6,500 assignments, it has extensive experience in aligning financial profiles with rating expectations.

Its strong network across rating agencies and financial institutions enables better strategic positioning during both rating and negotiation stages.

The proprietary Prepare, Position, Protect approach ensures that companies are not only financially ready but also presented in the most effective manner.

A no-cost initial assessment helps CFOs identify rating gaps and quantify potential interest savings before taking strategic decisions.

Each engagement is tailored to align with the company’s industry dynamics, financial structure, and growth objectives.

The Bottom Line

For CFOs in Mumbai, credit rating is more than a report.

It is a negotiation tool, a cost-control mechanism, and a hedge against uncertainty.

With the right strategy and advisory support, it can significantly improve borrowing outcomes in an evolving interest rate environment.