Types of Credit Ratings in India : Long-Term, Short-Term, Bank Loan, Structured Finance & More

By: admin

Articles

Introduction

Credit ratings are not uniform, they vary depending on the type of instrument, tenure, and risk profile. Whether it’s a short-term commercial loan, a long-term bond, or a structured finance product, each requires a distinct type of rating.

FinMen Advisors, India’s Largest Credit Rating Advisory & Leading IPO Advisory firm, explains the major types of credit ratings in India and why they matter for your financing decisions.

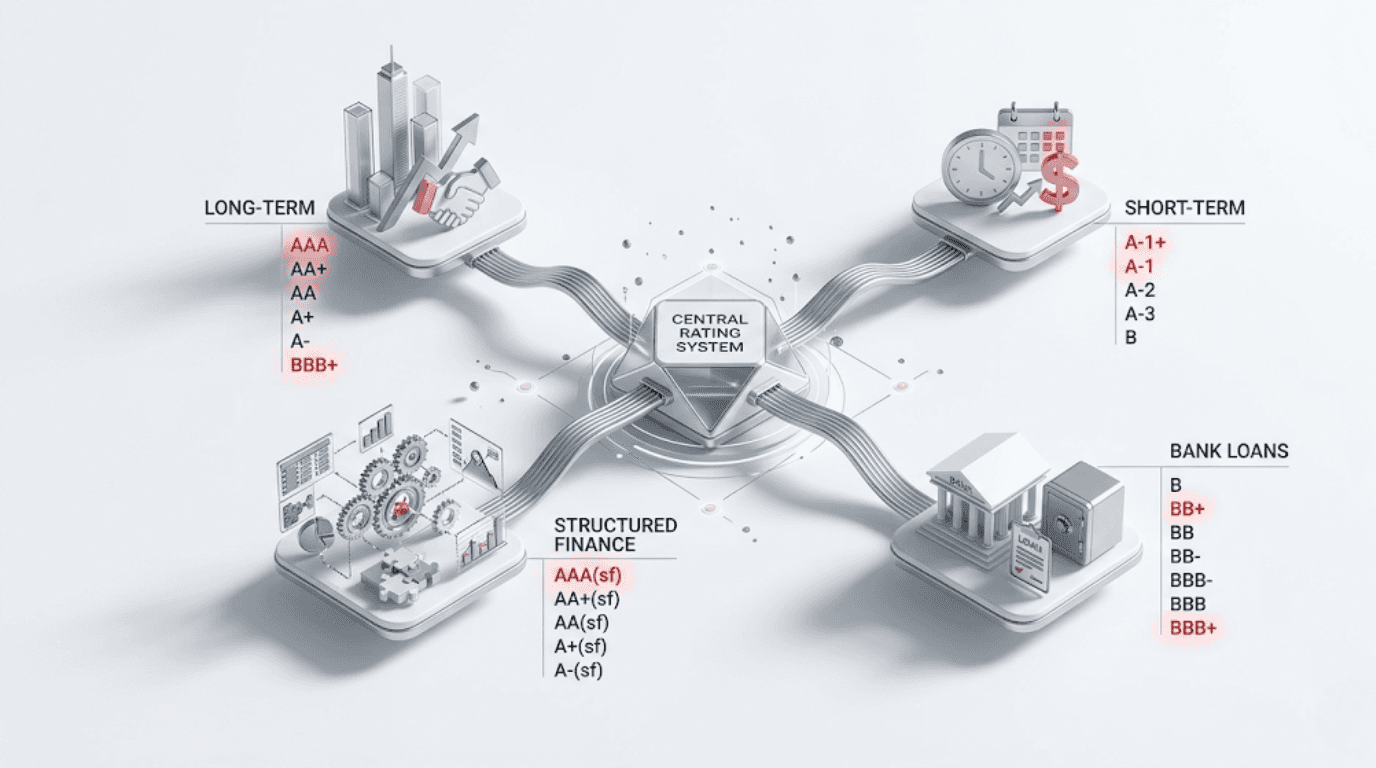

Major Types of Credit Ratings

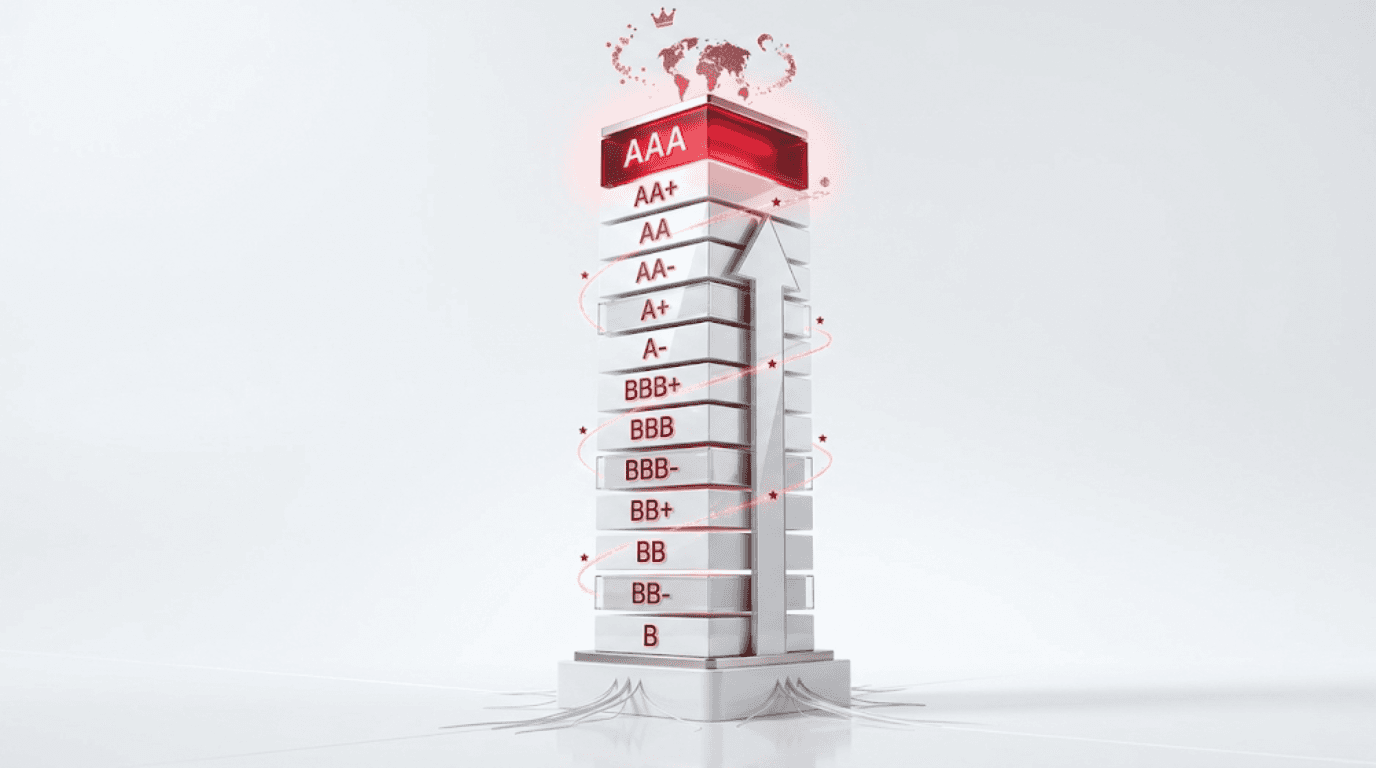

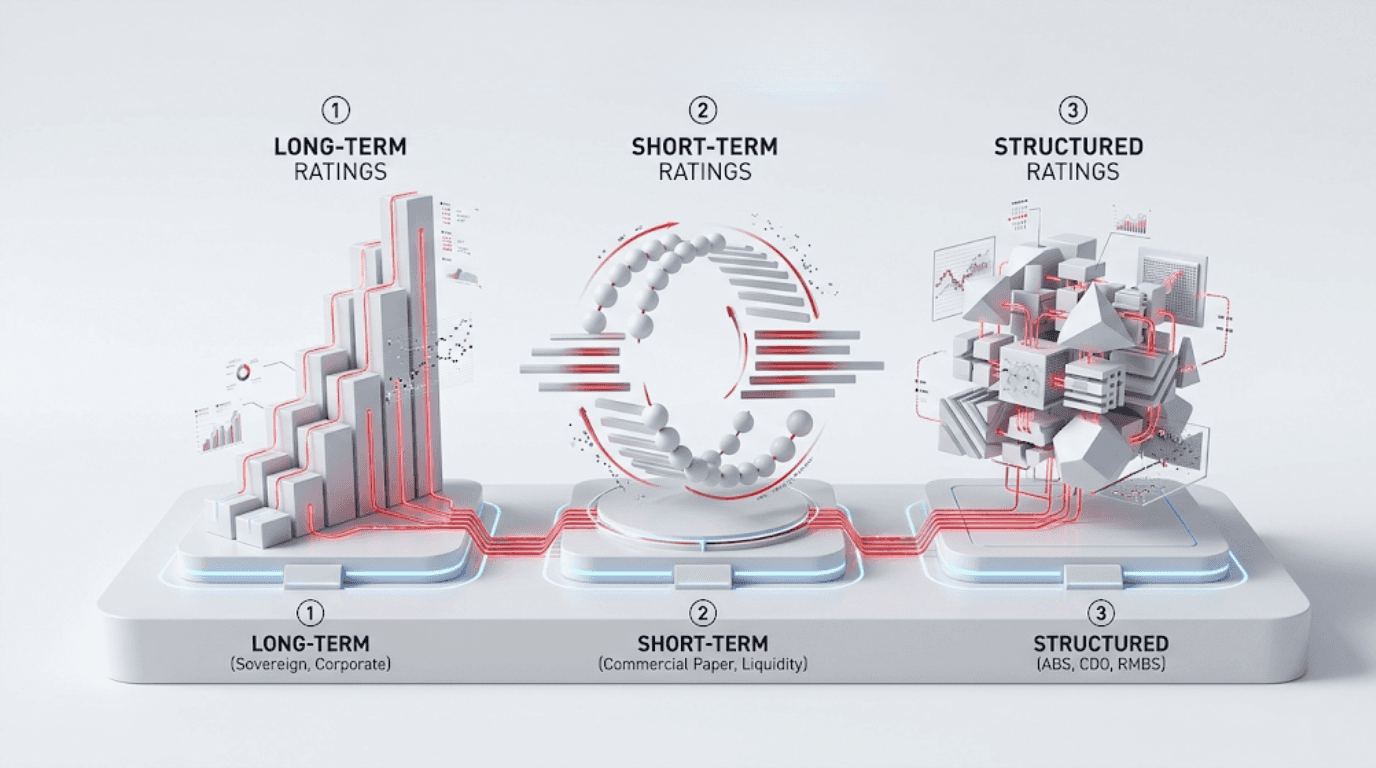

1. Long-Term Credit Ratings

Apply to obligations with maturities greater than one year, such as long-term bonds, term loans, and debentures.

Ratings usually follow scales like AAA, AA, A, BBB, BB, B, with AAA indicating the highest degree of safety.

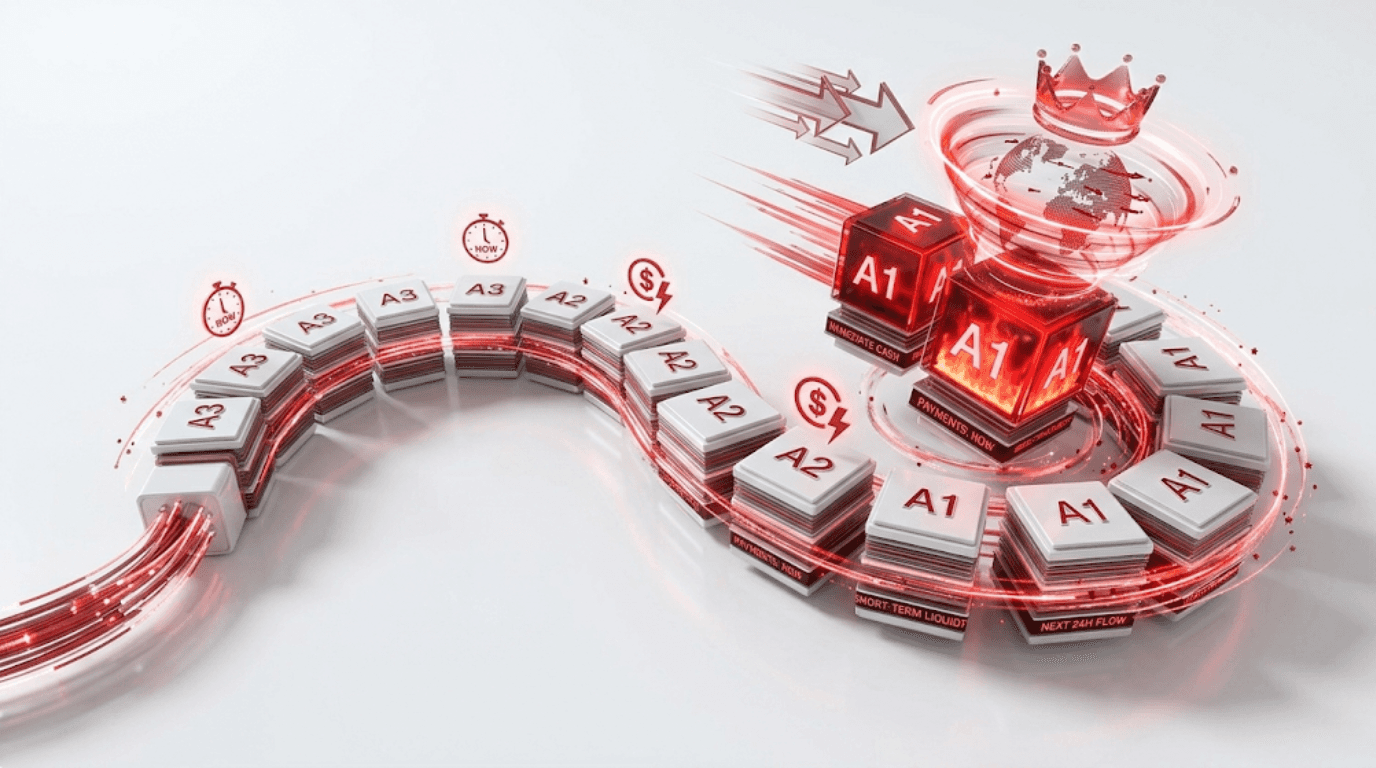

2. Short-Term Credit Ratings

Cover instruments with maturities of one year or less, like commercial paper (CP), certificates of deposit (CDs), and short-term borrowings.

Common scales include A1, A2, A3, A4, etc., with A1 being the highest.

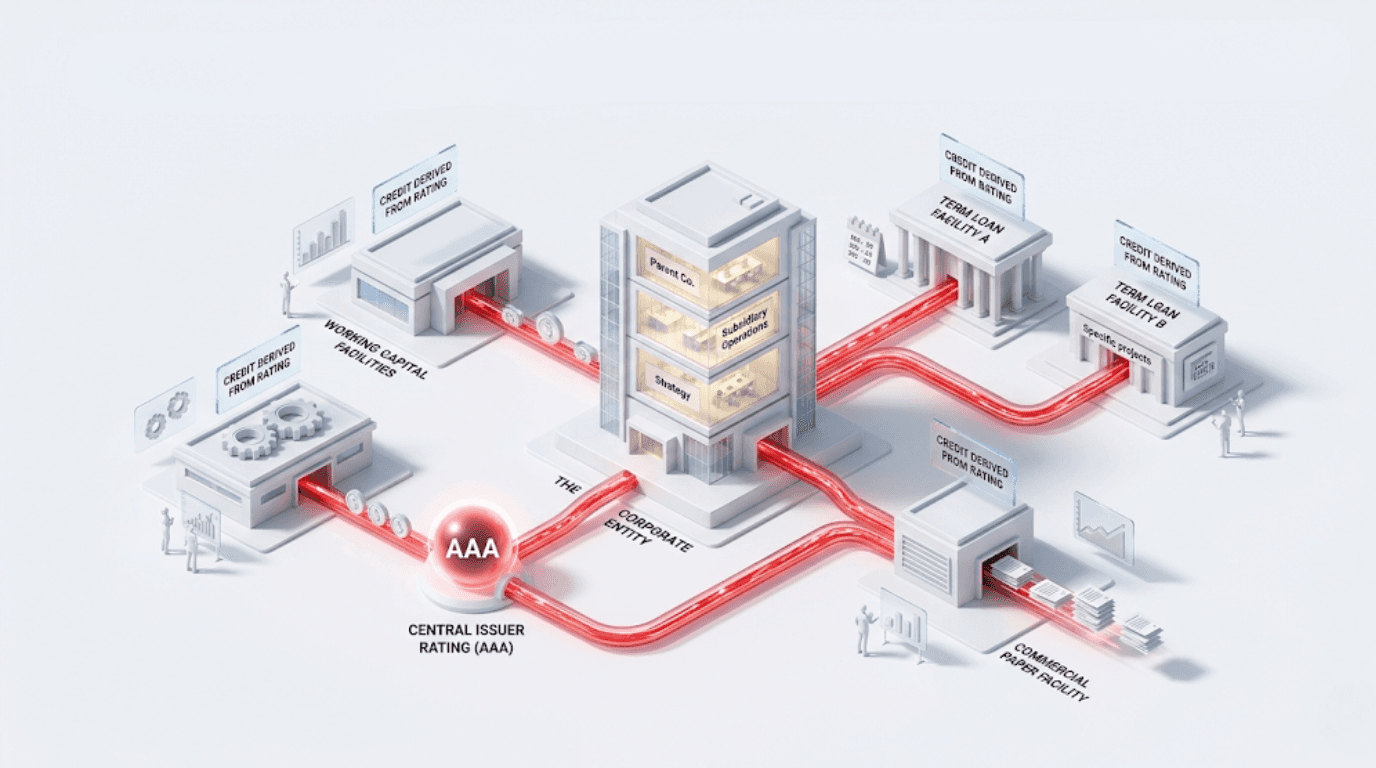

3. Bank Loan & Issuer Ratings

Bank loan ratings assess credit risk for facilities such as working capital loans or term loans.

Issuer ratings evaluate the overall creditworthiness of a company across all obligations, not just a single instrument.

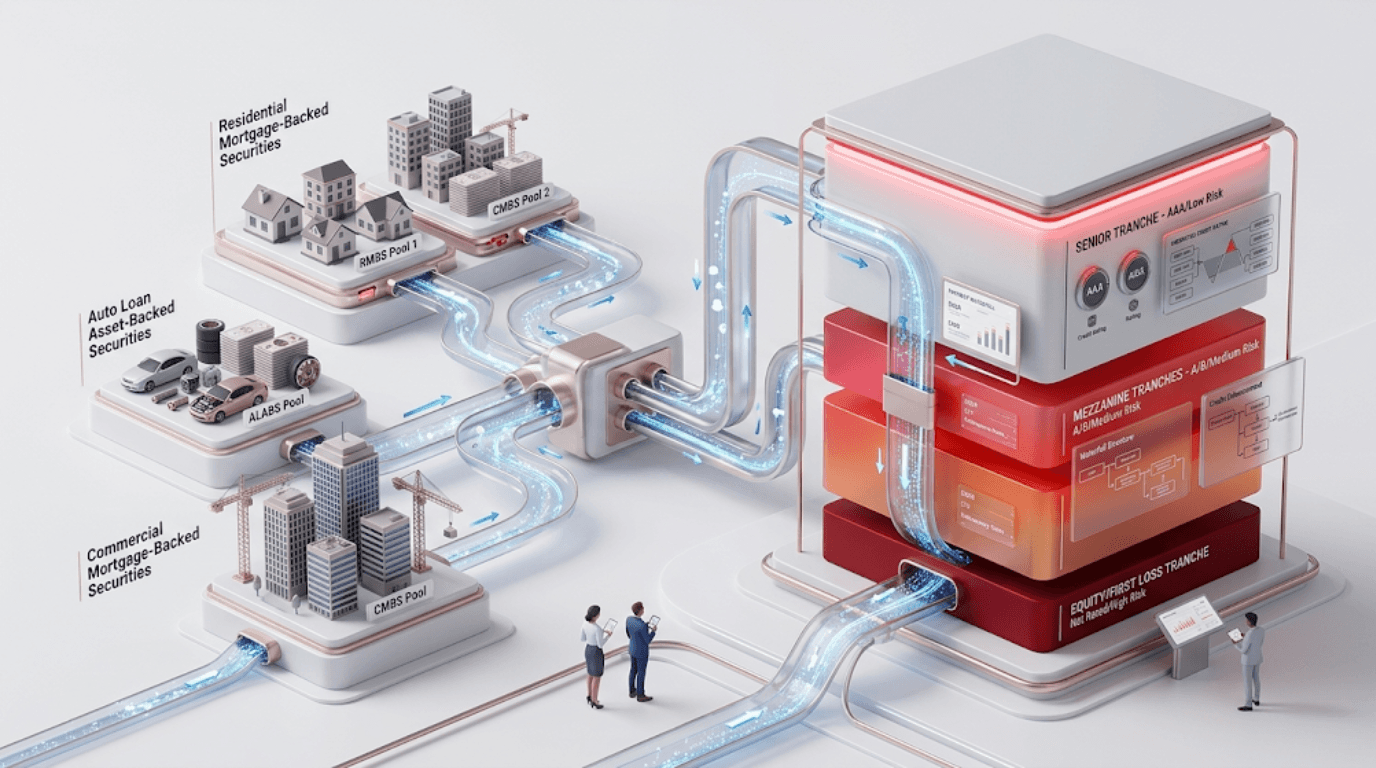

4. Structured Finance Ratings

Assigned to complex instruments pooling different assets, such as mortgage-backed securities (MBS), asset-backed securities (ABS), or securitization pass-through certificates (PTCs).

Factors include the quality of underlying assets, servicing of cash flows, and the presence of credit enhancements.

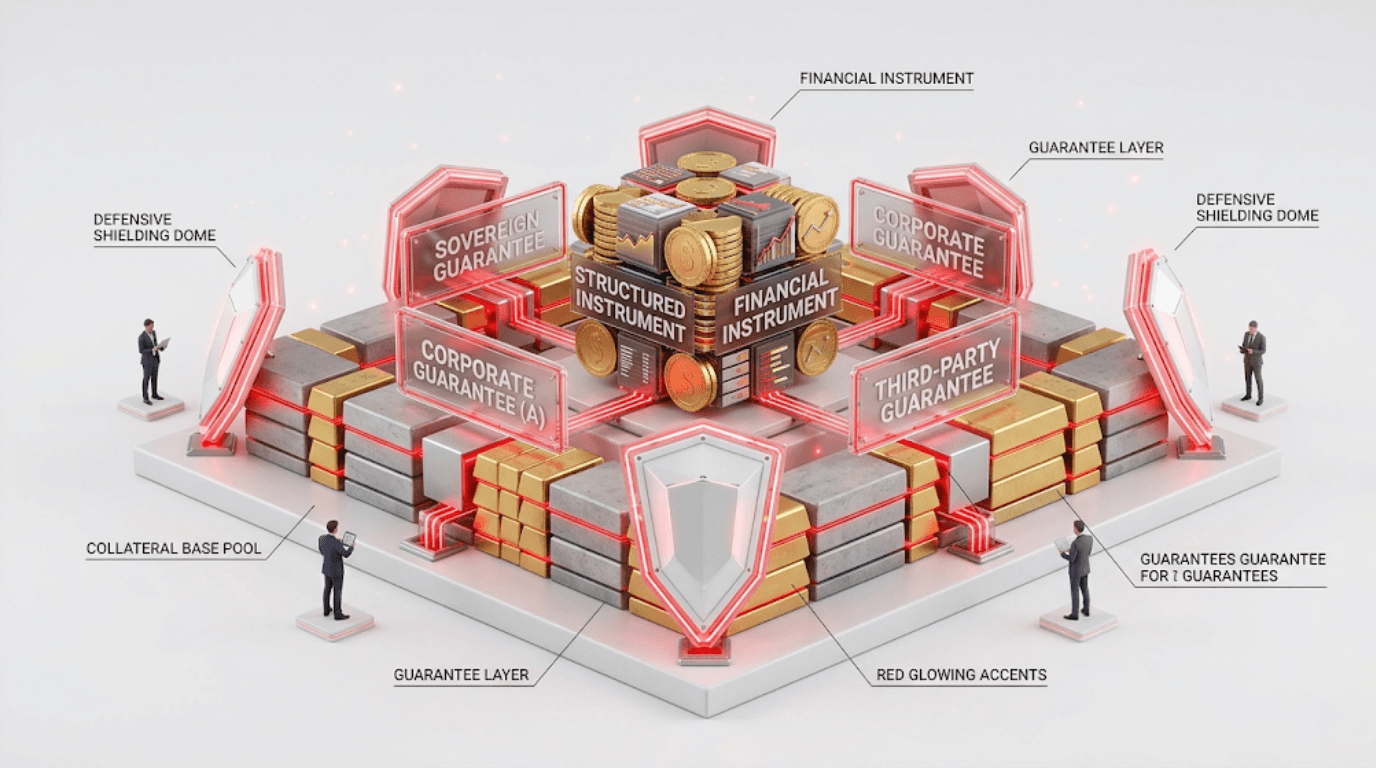

5. Credit Enhancement & Structured Obligation Ratings

Some instruments are backed by guarantees, collateral, or external support.

Agencies use suffixes like (SO) for Structured Obligation or (CE) for Credit Enhancement, signaling improved safety due to external support.

Why Different Ratings Matter for Businesses

Tailored financing: Each rating type applies to different borrowing needs.

Cost of funds: A stronger rating lowers interest costs; structured finance may improve access to investors.

Investor confidence: Different investors rely on specific ratings for decision-making.

Regulatory compliance: Some instruments cannot be issued without appropriate ratings.

FinMen Advisors’ Role in Navigating Rating Types

As India’s leading credit rating advisory firm, FinMen Advisors helps businesses:

Identify which rating type suits their borrowing/investment plans.

Prepare robust documentation for rating agencies.

Evaluate credit enhancement options for better outcomes.

Select the right CRA and rating structure for specific instruments.

Disclaimer: FinMen Advisors provides advisory support only and does not guarantee any particular credit rating outcome.

FAQs

Q1: What is the difference between a short-term and long-term rating?

A1: Short-term ratings apply to obligations up to one year and focus on liquidity, while long-term ratings assess credit risk for obligations exceeding one year.

Q2: What does a structured obligation (SO) rating mean?

A2: It applies to instruments where repayment is supported by structures like securitization or guarantees, beyond just the issuer’s credit strength.

Q3: What is credit enhancement (CE)?

A3: CE refers to mechanisms like collateral, guarantees, or external support that improve an instrument’s safety and rating.

Q4: If my company issues bonds, which rating do I need?

A4: Bonds typically require long-term ratings, though structured or credit-enhanced bonds may also carry SO/CE ratings.

Conclusion

Understanding the different types of credit ratings is crucial for businesses looking to raise funds effectively. From short-term loans to structured finance products, each rating type has unique implications for cost, compliance, and investor trust.

FinMen Advisors, India’s Largest Credit Rating Advisory & Leading IPO Advisory firm, supports businesses in choosing the right rating path, preparing thoroughly, and presenting their case effectively to credit rating agencies.