Shadow Ratings for Mumbai Fintechs: Bridging the Gap Between Equity and Institutional Debt

By: admin

Articles

Shadow Ratings for Mumbai Fintechs: Bridging the Gap Between Equity and Institutional Debt

In the evolving financial ecosystem of Mumbai, fintech companies are redefining how capital is accessed, deployed, and scaled.

Over the last decade, most fintechs have relied heavily on equity capital to fuel growth. However, as these companies mature, the focus gradually shifts toward institutional debt to optimize cost of capital and improve return on equity.

This transition is not automatic.

It requires one critical enabler: creditworthiness in the eyes of lenders.

And this is where shadow rating becomes a strategic bridge between equity-funded growth and debt-funded scalability.

The Fintech Funding Shift

Early-stage fintechs typically depend on:

Venture capital

Private equity

Founder funding

These sources prioritize growth, scalability, and market capture.

However, as fintechs move toward stability, they need:

Lower-cost capital

Predictable funding sources

Scalable debt structures

Institutional lenders, including banks and NBFCs, step in at this stage.

But unlike equity investors, lenders prioritize:

Risk management

Cash flow visibility

Capital protection

This creates a gap between how fintechs are built and how they are evaluated for debt.

What is a Shadow Rating

A shadow rating is a pre-rating assessment that estimates how a fintech would be evaluated by a credit rating agency before formally applying for a rating.

It analyzes:

Financial performance

Business model sustainability

Portfolio quality

Liquidity and capital adequacy

Governance and risk frameworks

Most importantly, it answers:

“Are we ready to transition from equity confidence to debt credibility?”

Why Fintechs Face Unique Rating Challenges

Fintech companies differ significantly from traditional businesses.

They often have:

Rapid growth but limited profitability

High customer acquisition costs

Evolving business models

Technology-driven operations

Short operating track records

While these factors are acceptable in equity markets, they can raise concerns for lenders.

This leads to a critical challenge:

Strong fintechs may still receive conservative credit ratings if not properly positioned.

The Risk of Skipping Shadow Rating

Approaching rating agencies directly without preparation can result in:

Lower-than-expected ratings

Misinterpretation of business model

Underestimation of technology-driven strengths

Weak articulation of risk management practices

Once assigned, the rating becomes public and influences:

Borrowing cost

Investor perception

Future fundraising ability

How Shadow Rating Bridges the Gap

Shadow rating helps fintechs align their profile with lender expectations.

1. Converts Growth Story into Risk Narrative

Transforms high-growth metrics into sustainable financial indicators

2. Identifies Structural Gaps

Highlights areas such as profitability, liquidity, or governance that need improvement

3. Prepares for Lender Scrutiny

Ensures readiness for detailed due diligence

4. Improves Rating Outcome Probability

Aligns business profile with rating methodologies

5. Builds Confidence for Debt Raising

Enables fintechs to approach lenders with clarity and control

Why This Matters More in Mumbai

Fintechs based in Mumbai operate at the intersection of:

Financial services

Technology innovation

Institutional capital

They actively engage with:

Banks

NBFCs

Debt funds

Structured credit investors

In such an ecosystem:

Credit rating becomes a key credibility marker

Funding decisions are highly perception-driven

Preparation directly impacts capital access

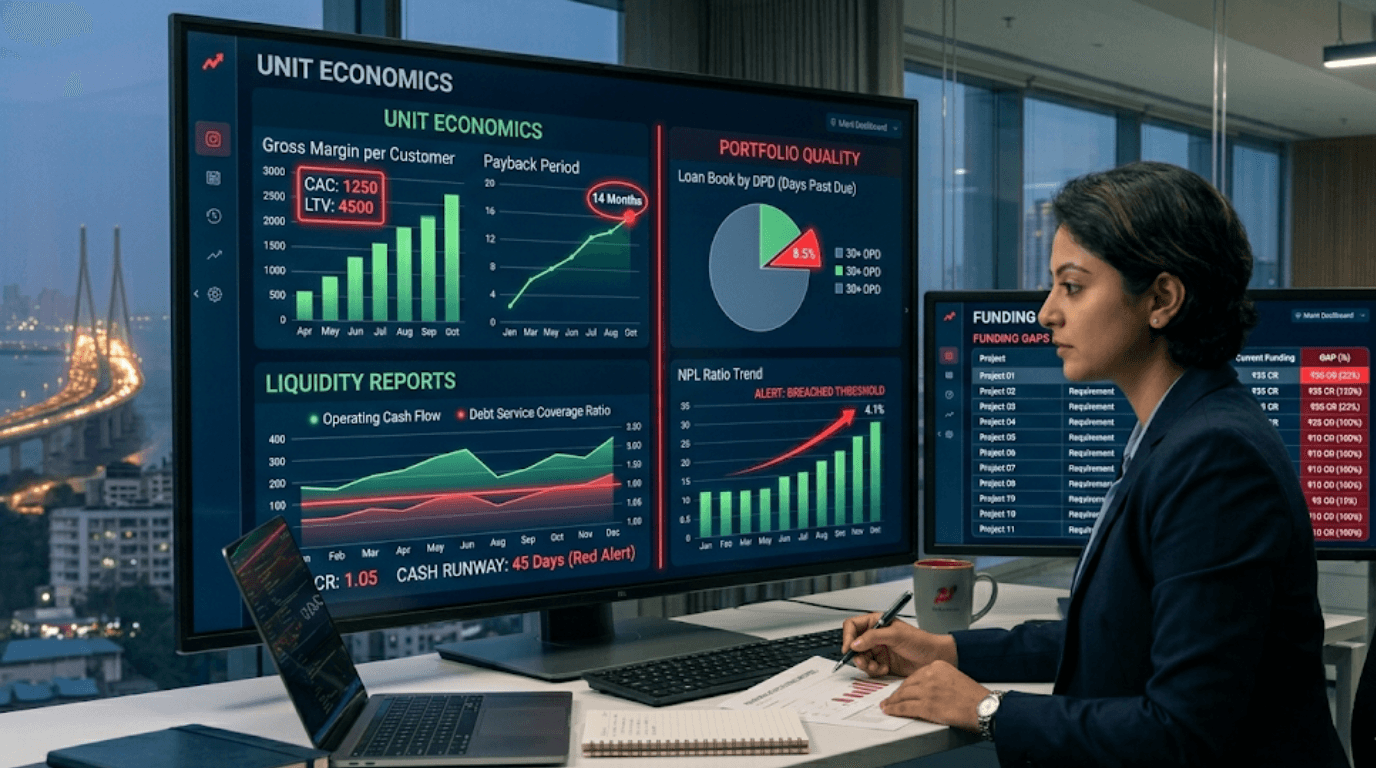

Key Areas Evaluated in a Fintech Shadow Rating

A structured shadow rating focuses on fintech-specific parameters:

Unit Economics

Customer acquisition cost versus lifetime value

Portfolio Quality

Delinquency levels and credit risk management

Capital Adequacy

Ability to absorb losses and sustain growth

Liquidity Position

Availability of funding buffers and cash flow visibility

Governance and Risk Frameworks

Strength of internal controls and underwriting processes

Scalability and Sustainability

Long-term viability of the business model

The Strategic Insight Most Fintech Founders Miss

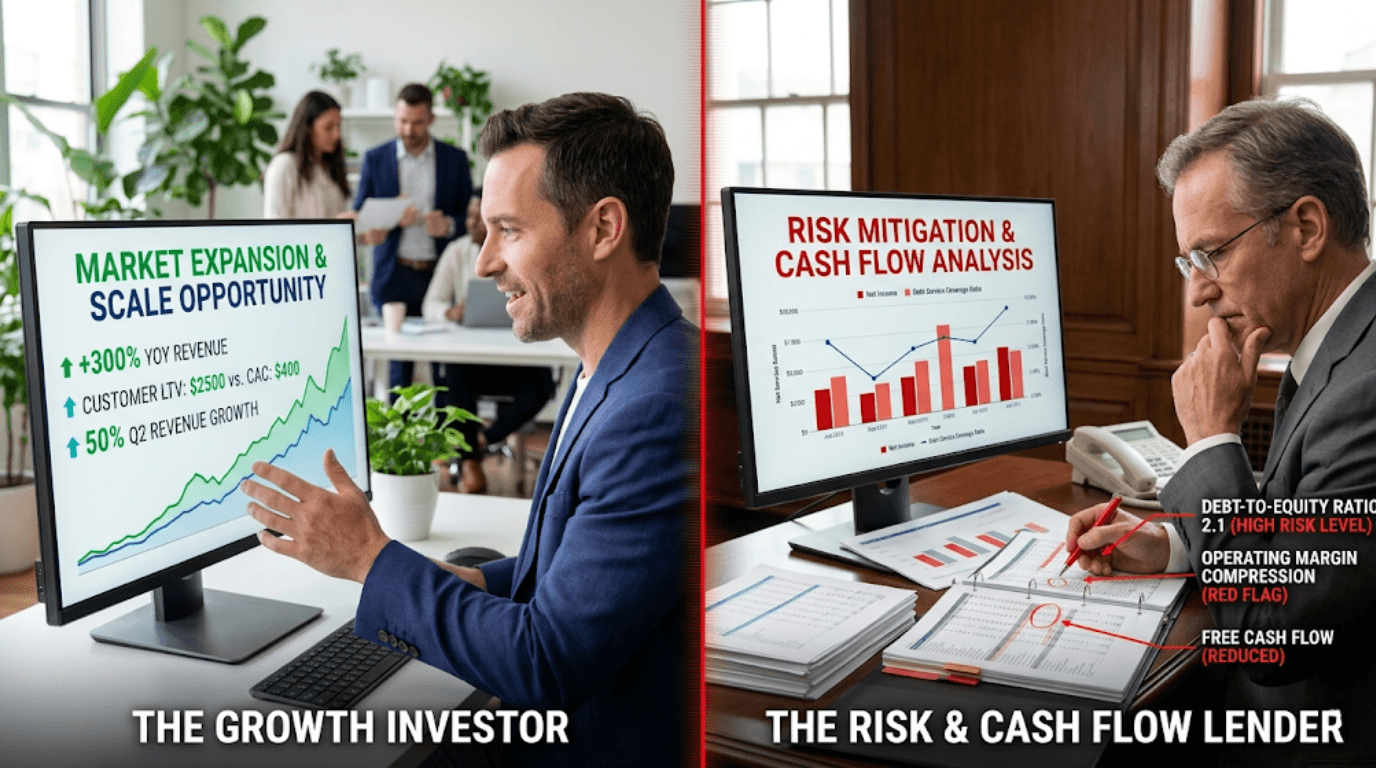

Equity investors back potential.

Lenders fund predictability.

Credit rating is the bridge between the two.

Two fintechs with similar growth trajectories can receive very different funding outcomes based on how well they translate growth into risk-adjusted stability.

A Practical Transition Strategy for Fintechs

Leading fintechs follow a structured approach:

Conduct a shadow rating assessment

Identify gaps between current profile and lender expectations

Strengthen financial and operational metrics

Build a robust risk and governance framework

Approach rating agencies and lenders with confidence

Conclusion: From Growth to Credibility

In a competitive hub like Mumbai, fintechs cannot rely on equity capital indefinitely.

The ability to access institutional debt at the right cost becomes a key differentiator.

Shadow rating enables fintechs to transition from growth-driven narratives to credibility-driven funding.

Why Companies Choose FinMen Advisors for Credit Rating Advisory

For fintechs, the challenge is not just obtaining a credit rating. It is ensuring that the rating accurately reflects the strength and scalability of the business model.

FinMen Advisors brings a structured and experience-driven approach to this transition.

With over 15 years of specialized expertise, the firm understands how emerging business models like fintech are evaluated by rating agencies and lenders.

Having executed more than 6,500 assignments, it has strong experience in conducting shadow assessments and preparing companies for institutional funding.

Its pan-India presence and relationships with rating agencies and financial institutions provide a strategic advantage during the rating process.

The Prepare, Position, Protect approach ensures that fintechs are not only financially ready but also strategically presented.

A no-cost initial assessment helps companies identify gaps in their credit profile and quantify their readiness for debt funding.

Each engagement is customized to align with the fintech’s business model, growth stage, and funding strategy.

The Bottom Line

For fintechs, the journey from equity to debt is not just a funding shift. It is a transformation in how the business is evaluated.

Shadow rating is the bridge that makes this transition smoother, more predictable, and more successful.

With the right strategy and advisory support, fintechs can unlock institutional capital, optimize cost of funds, and scale sustainably.