Rating vs. Security: How a Strong Rating Reduces Collateral Requirements at Mumbai’s Top Banks

By: admin

Articles

Rating vs. Security: How a Strong Rating Reduces Collateral Requirements at Mumbai’s Top Banks

In the lending ecosystem of Mumbai, one question consistently comes up during credit discussions:

“How much collateral do we need to provide?”

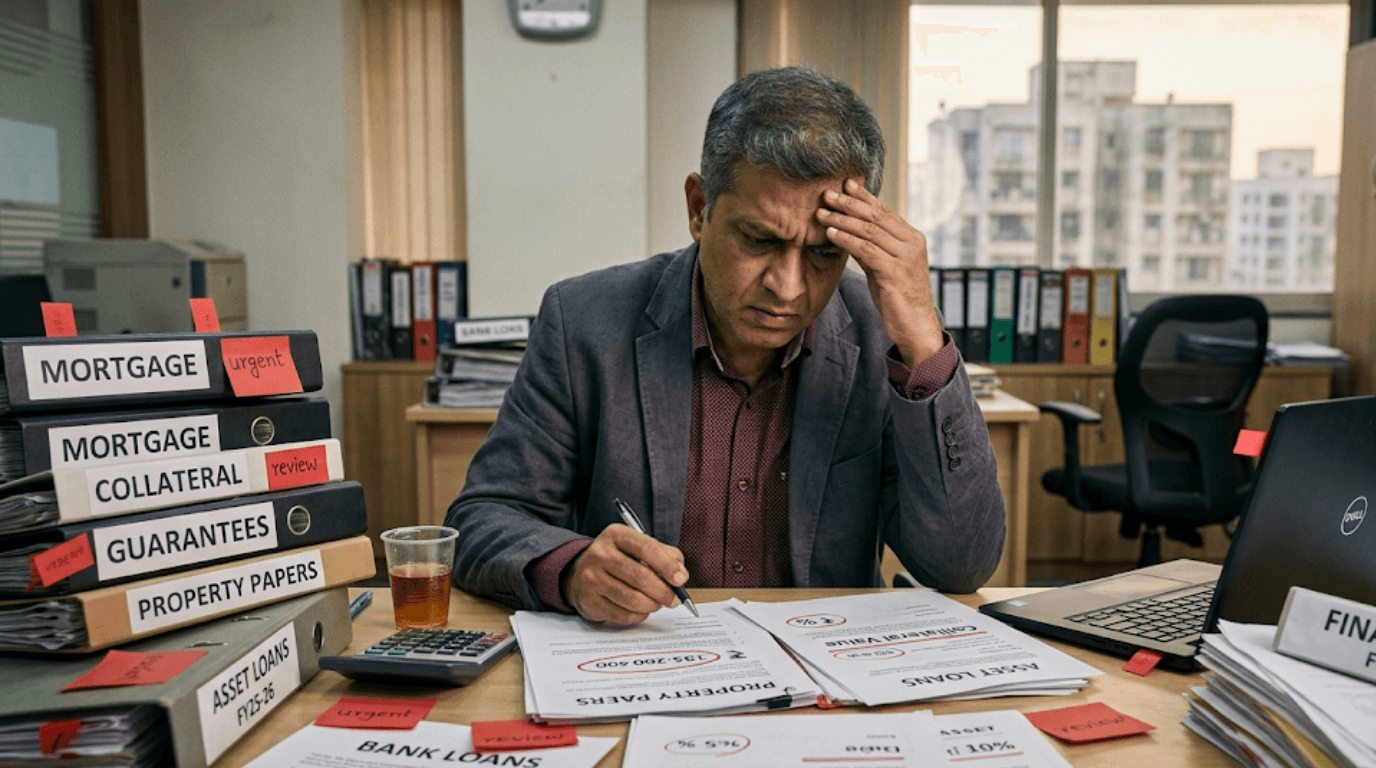

For many businesses, especially mid-sized companies, collateral often becomes a bottleneck—restricting borrowing capacity and locking valuable assets.

However, what many CFOs and promoters overlook is this:

Collateral is not just a function of asset availability. It is a function of risk perception.

And that perception is significantly influenced by credit rating.

The Traditional View: Collateral as a Safety Net

Banks typically seek collateral to:

Mitigate default risk

Secure exposure

Ensure recovery in case of stress

This leads to common requirements such as:

Property mortgages

Fixed asset hypothecation

Personal or corporate guarantees

For lower-rated or unrated companies, lenders rely heavily on collateral because confidence in repayment capacity is limited.

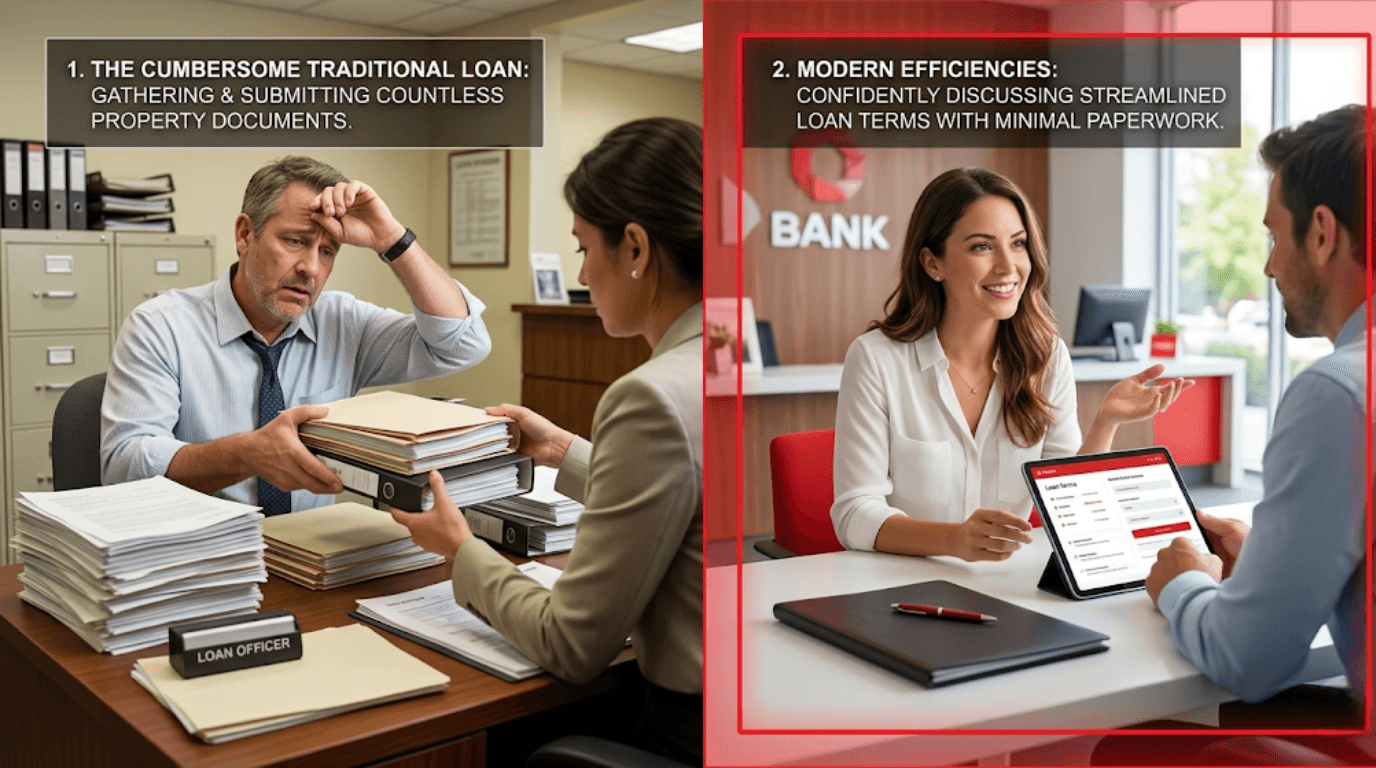

The Shift: From Asset-Backed to Risk-Based Lending

Modern banking, especially in a competitive market like Mumbai, is increasingly moving toward risk-based lending.

This means:

Stronger companies are evaluated more on cash flows than assets

Creditworthiness plays a bigger role than collateral

Credit rating becomes a critical decision-making tool, helping banks assess:

Probability of default

Financial discipline

Stability of operations

A higher rating signals lower risk, which reduces the need for heavy collateral backing.

How Credit Rating Impacts Collateral Requirements

A strong credit rating influences lending structure in multiple ways.

Reduced Collateral Coverage Ratio

Banks may require lower collateral value relative to loan exposure

Shift Toward Cash Flow-Based Lending

Greater reliance on business performance rather than asset backing

Flexibility in Security Structures

Possibility of partial collateral or unsecured components

Lower Dependence on Personal Guarantees

Promoters may not need to over-leverage personal assets

A Practical Illustration

Consider two companies with similar borrowing needs:

Company A

Rating: BBB

Higher perceived risk

Bank requires 100 percent or higher collateral coverage

Company B

Rating: A

Lower perceived risk

Bank may reduce collateral requirement significantly or structure part of the loan unsecured

The difference is not just financial. It is strategic.

Company B retains asset flexibility, enabling:

Additional borrowing capacity

Better capital allocation

Reduced asset encumbrance

Why This Matters More in Mumbai

Businesses in Mumbai operate in a highly competitive credit environment with access to:

Multiple banks and NBFCs

Structured financing options

Faster refinancing cycles

In such a market, lenders compete for high-quality borrowers.

This creates an important shift:

Well-rated companies can negotiate not just interest rates, but also collateral terms.

Beyond Collateral: Additional Advantages of a Strong Rating

A better credit rating enhances overall borrowing efficiency.

Improved Loan Structuring

More flexibility in designing funding arrangements

Faster Approvals

Lower perceived risk accelerates credit decisions

Enhanced Credibility

Stronger trust with lenders and financial institutions

Better Access to Unsecured Funding

Higher probability of obtaining partially or fully unsecured facilities

What Holds Companies Back

Many companies continue to provide excessive collateral due to:

Lack of awareness about rating impact

Weak financial presentation

Inefficient structuring of borrowing proposals

Underestimation of qualitative strengths

In many cases, the issue is not lack of assets. It is lack of positioning.

Strategic Levers to Reduce Collateral Dependency

Companies looking to optimize collateral requirements should focus on:

Strengthening Financial Metrics

Improving leverage, coverage ratios, and profitability

Building Predictable Cash Flows

Ensuring consistency in revenue and collections

Enhancing Transparency

Maintaining strong reporting and disclosure practices

Improving Credit Rating

Actively working toward a higher rating profile

Structuring the Right Narrative

Clearly communicating strengths to lenders and rating agencies

The Strategic Insight Most CFOs Miss

Collateral is not just protection for the bank. It is a reflection of trust.

Higher trust reduces the need for security.

Credit rating directly influences that trust.

Two companies with similar assets can face completely different collateral requirements simply because one is better rated and better positioned.

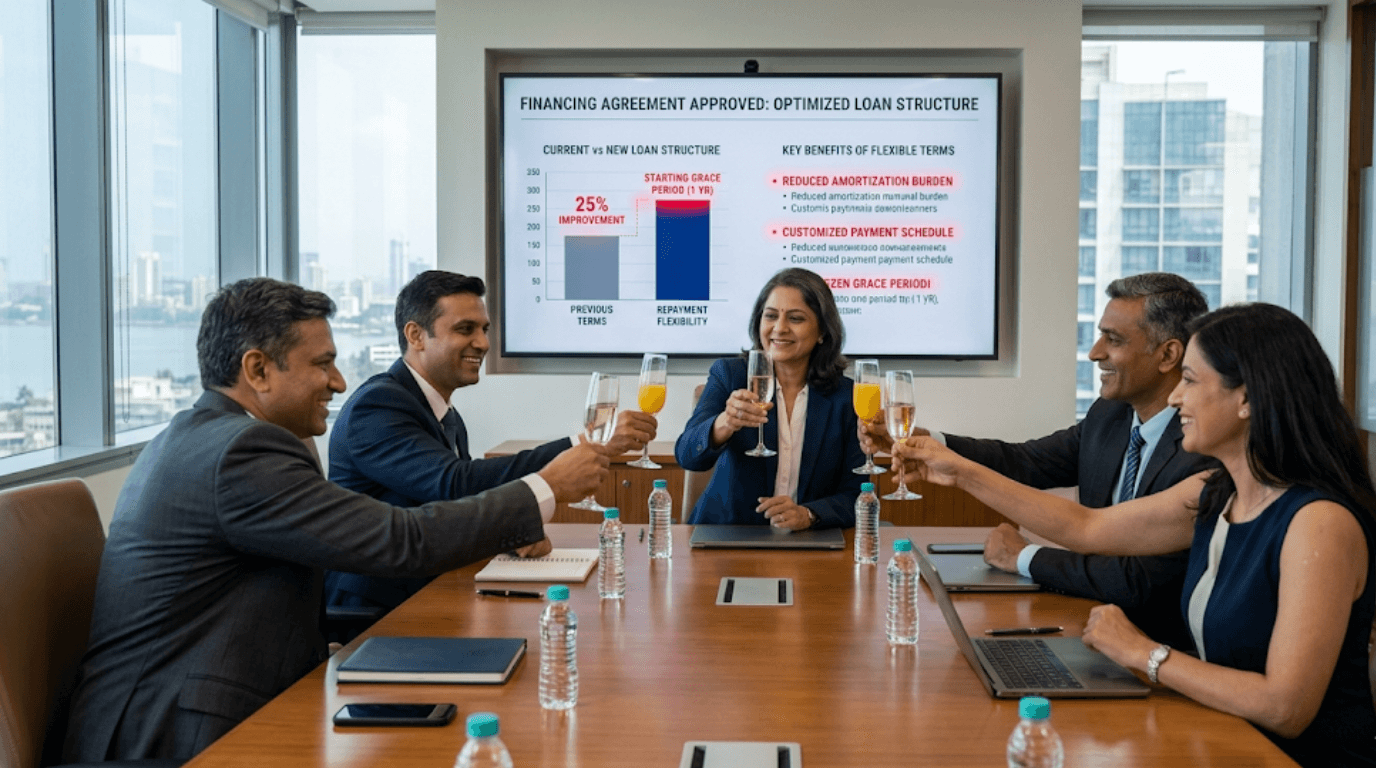

Conclusion: Freeing Up Assets for Growth

In a city like Mumbai, where capital efficiency drives growth, locking assets as collateral comes at a cost.

Reducing collateral dependency allows businesses to:

Preserve asset flexibility

Improve return on capital

Unlock additional funding opportunities

A strong credit rating does not just reduce borrowing cost. It frees up your balance sheet.

Why Companies Choose FinMen Advisors for Credit Rating Advisory

Optimizing collateral structures requires more than financial strength. It requires the ability to align risk perception with actual business capability.

FinMen Advisors brings a structured and experience-driven approach to this process.

With over 15 years of specialized expertise, the firm understands how credit rating influences both pricing and collateral requirements in bank financing.

Having executed more than 6,500 assignments, it has strong experience in positioning companies for improved credit outcomes.

Its pan-India presence and relationships with rating agencies and financial institutions provide a strategic advantage during lending negotiations.

The Prepare, Position, Protect approach ensures that companies are not only financially ready but also presented in the most effective way.

A no-cost initial assessment helps businesses identify gaps in their credit profile and quantify potential benefits in terms of reduced collateral and improved funding access.

Each engagement is tailored to align with the company’s financial structure, industry dynamics, and growth strategy.

The Bottom Line

For CFOs, collateral is not just a requirement. It is a cost.

Credit rating is one of the most powerful tools to reduce that cost.

With the right strategy and advisory support, businesses can move from asset-heavy borrowing to efficient, trust-driven financing structures.